Critical Mineras and EU-Africa collaboration - need for reset

Opinion column by Julius Gatune

The green transition and digitalization, the so-called twin transition, are creating significant demand for minerals needed to build batteries, windmills, digital devices, etc. The International Energy Agency (IEA) has compiled a list of 37 minerals and metals important for the green transition (IEA, 2024). At the same time, these minerals are found in a few countries and also processed by a few countries, making the supply chains of these minerals vulnerable to disruption. For these reasons, the minerals are collectively now referred to as Critical Raw Materials (CRM)1.

Depending on countries’ industrial needs, the list of critical raw materials varies. Many countries also include minerals needed for the defense industry as part of critical raw materials. As a result, different countries, industries, and other stakeholders have different lists of critical materials, though there are many minerals that are perceived as critical across many countries. The list of CRMs also changes over time as the dynamics driving criticality change. The EU has a list of 34 CRMs as of 2023.2

The rising tensions between the collective West and China which currently has a dominant position in CRM processing capacity (refining more than 50% of global lithium, 85% of rare-earth elements, and 95% of manganese (IEA, 2023; Cordier, 2024; Fleck, 2024)) has brought urgency in the West to develop new supply chains and reduce dependence on China. The concerns for security of supply have seen a growing shift toward nationalist economic practices within Western industrial policy (Blanco and Middleton, 2024). This has seen a concerted effort to build new supply chains based on partnerships with countries seen as friendly. One example in the US is the Mineral Security Partnership (MSP) that aims to diversify the sourcing of critical minerals away from China and give priority to allies.3

The boom in CRMs has potential for accelerating African economic transformation. Africa is estimated to hold approximately 30% of the world’s proven CRM supplies and has near dominance in some CRMs. For example, the Democratic Republic of the Congo (DRC) accounts for approximately 74% of global cobalt production while three African countries account for over 60% of global manganese production (IMF, 2024). However, most of Africa’s CRMs are exported in their raw form. For example, the DRC exports approximately 97% of its cobalt, mostly unprocessed, to China (IEA, 2019). Only 2% of exports of these minerals end up in other African countries. At the same time, CRM wealth is driving conflict in Congo DRC, underscoring the dark side of mineral resources wealth, the so-called resource curse.

To ensure mineral riches translate to improved livelihoods and drive the needed transformation, many countries in Africa have implemented strategies mainly focused in increasing local content (LC) in mining activities (local suppliers and local employment) and increasing local processing (local value addition (LVA)). Beyond LC and LVA, which focus on minerals in general, some countries have also promulgated CRM strategies. The impetus has ranged from resource nationalism (local ownership) to the desire to capture more revenues, to ambitions of becoming green industrialization hubs (Gatune and Adjaye 2025). While it is too early to assess the effectiveness of measures, a key challenge across all countries is a weak industrial ecosystem, in particular energy, skills, and a weak private sector (Gatune 2024, Gatune and Adjaye 2025).

Africa is now the focus, as countries seek to secure critical minerals. This has seen a recent increase in multilateral, bilateral, or state-to-state agreements between African countries and Western countries aimed at securing access to CRMs. Africa today has over 100 mineral partnership agreements with countries in the Global North, the Middle East, and Asia (Bueter et. al. 2024). An example is the 2023 Memorandum of Understanding (MoU) on the development of the Lobito corridor, signed by Zambia and the Democratic Republic of Congo on the one hand and the European Union (EU), the United States (US) on the other hand (US Embassy in Zambia, 2023). However, it has been pointed out that these agreements risk perpetuating past extractive models because they do not adequately address local priorities like governance, economic transformation, community participation, and environmental sustainability (Bueter et. al. 2024). Schulze (2025) argues that the EU and the US both seek to strengthen domestic value creation, further perpetuating the old model of Africa as an exporter of commodities. And that the emerging minerals transport corridor projects risk prioritizing external mineral needs over African industrial development and regional integration (Ecofin, 2025b). For CRM to translate to a win-win collaboration, a more deliberate approach is needed that ensures Africa’s industrialisation is a central part of the emerging agreements.

Rethinking EU-Africa CRM collaboration

The EU's strategy for diversifying its supply chain includes establishing raw materials partnerships with various countries. The EU’s agreements typically include provisions for establishing a joint roadmap to steer future cooperation and emphasize partnerships between producer and consumer countries (Beuter et. al. 2024). The EU is also in the process of signing bilateral agreements with several African countries and has already bilateral agreements with Namibia (EC, 2022), the DRC (EC, 2023), Rwanda (EC, 2025a), and Zambia, while negotiations have also begun with South Africa (EC, 2025b).

Africa presents the EU with a crucial advantage as it seeks to secure a supply of CRMs and advance its green industrialisation drive. The geographical proximity results in short supply chains. Europe has a strong presence and longstanding engagement in Africa, shaped by historical ties.

This EU partnership model, being promoted in Africa, expects the private sector to take the lead in driving investment, bolstered by bilateral investment treaties. However, given the high levels of risk associated with extractive projects, these investments have not materialized as expected. For example, the EU’s strategic partnership with Namibia has not significantly stimulated European investment in the country’s critical mineral sector despite Namibia’s favourable political stability and investment environment (Beuter et. al. 2024). Similarly, Zambia has not attracted private sector investments despite several projects being granted strategic project status under the EU CRMA.

So while the EU and Africa are especially placed to drive a win-win proposition, as some building blocks are in place, this will require rethinking of the current arrangements. Some potential approaches include:

- Regional Approach: For Africa to fully benefit from increased interest in its CRM wealth, it needs to take a regional approach using the emerging corridors as the vectors for regional value chains. For example, for Africa to create a battery cluster, it will need to harness graphite from Mozambique, Tanzania, and Malawi, and Copper and Cobalt from Zambia and the DRC. The Lobito, Nacala, and Tazara railway corridors provide a natural backbone for developing such a cluster. The current EU approach of signing agreements with countries should be replaced by a multilateral approach that seeks to develop industry clusters. However, it seems like the current approach is based on the extraction model, where the EU extracts the minerals for developing industry clusters elsewhere.

- Geological Collaboration: The known African mineral wealth is far below its potential and could easily grow fivefold. Collier and Laroche (2015) point out that resource extraction per square kilometer in Africa is about 20% of the OECD average4. This situation is largely driven by the generally low level of geological knowledge in many countries5. EU support in developing capacity for geological exploration can have a huge impact. Given that mineral belts span boundaries, regional geological surveys will have greater payoffs than working with countries.

- Private Sector Development: A weak supplier base is also a challenge in driving green industrialisation. For example, 99% of all Mozambican enterprises are microenterprises (AfDB et al., 2016). As mining is dominated by large multinational corporations, it is very difficult for small enterprises to be part of the supplier networks of these big companies. Greater attention should be devoted to enterprises needed to build a thriving industrial ecosystem. One way the EU can help is to incentivize EU medium-scale enterprises to invest in Africa. Medium enterprises can easily interface with large MNCs as well as small African enterprises, helping to facilitate the flow of know-how, technology, and resources to smaller firms and stimulate their upgrading.

- EU-Africa Trade: The EU already has a free trade agreement with Morocco that allows goods manufactured in Morocco easy access to the EU market. Indeed, that arrangement has led EU companies such as Stellantis to manufacture electric cars in Morocco for the EU market. This arrangement should be scaled up to the continental level, rather than bilateral. The EU should establish a free trade agreement with the African Continental Free Trade Area (AfCFTA). This can have huge benefits in attracting investments in green industrialization, as investors will not only have access to African markets but also to EU markets.

- Circular Migration: While migration remains a controversial topic in the EU, migration is a reality we cannot ignore, as there is a labour shortage in some sectors in Europe. CRMs can be leveraged to create a circular migration that can benefit both regions. Access to CRMs can be tied to efforts to build green skills in Africa by strengthening the capacity of training institutions. Europe can leverage this to address labour and skills gaps. The same people, after a short period and further training in entrepreneurship, can return to Africa to build green businesses and help Africa’s green industrialization. Returnees can also be given funding to establish a green business.

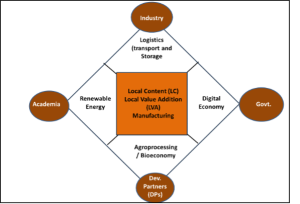

- Stimulate a broad transformation agenda: Achieving economic transformation lies in building strong clusters of interrelated industries based on the local endowments and national ambitions. While critical minerals are the key resource of interest, agriculture is the foundation of many economies in Africa. The CRM driven transport corridors should be a backbone for manufacturing clusters (especially agroprocessing), industrial parks, free-trade zones, and integrated logistics. This will be best achieved through building skills, building entrepreneurship, and also a strong innovation ecosystem. The model that will support this is a quadruple helix partnership (Q-Helix) where governments, the private sector, academia, and development partners (including civil society) work closely together to drive local economic development (LED). This is shown in Figure 1.

Figure 1: Potential model for a CRM driven corridor development

EU needs to revisit its approach to Africa regarding critical minerals and see its green transitions and African green industrialization strategy as two sides of teh same coin. A holistic rather than bilateral approach is needed.

About the Author - Dr. Julius Gatune

Dr Julius Gatune is a Senior Project Consultant and Assistant Professor with the Maastricht University-Maastricht School of Management (MSM), Netherlands. He is also the UNESCO Chair of Futures and Visiting Associate Professor at the Dedan Kimathi University of Science and Technology (DeKUT). He is also a senior fellow with the African Center for Economic Transformation (ACET) a pan-African think tank. He has also been a management consultant with McKinsey & Co and a researcher at Pardee centers for Futures studies at the University of Denver and at Boston University and an analyst at the RAND corporation. He holds a Ph. D in Policy Analysis for the Pardee RAND Graduate School and Masters in Computer Science from the University of Cambridge, UK. He also holds a Bachelor of Science in Civil Engineering (First Class Honors) and an MBA from the University of Nairobi, Kenya. His areas of interest include economic transformation, institutional development, 4th Industrial Revolution, Green Economy, foresight, innovation, agricultural value chains, and extractive industries governance.

Footnotes:

- criticality is of raw materials is based on the likelihood of a supply disruption of a material and the vulnerability of a system (e.g., a national economy, technology, or company) to this disruption( Schrijvers et.al. 2020). This is a function of the availability of material (a function of geology and investments), potential control of supply key producers, and other supply disruption challenges

- European Commission, Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs. (2023). Study on the critical raw materials for the EU 2023: Final report. Publications Office of the European Union. https://doi.org/10.2873/725585

- The key partners are Canada, Australia, Finland, France, Germany, Japan, South Korea, Sweden, the United Kingdom and the European Commission. Note that recent MSP working meetings have included representatives from Tanzania, Mozambique, Namibia, DRC, and Zambia.

- Mineral assets of sub-Saharan Africa are worth about USD 45,000 per square km. In comparison, known subsoil assets in the OECD are estimated at USD 265,000 per square km (Collier and Laroche, 2015).

- For example, about 45% of Zambia’s land remains unmapped, and 55% was mapped 25 years ago. Macroeconomic challenges have deterred private exploration, leaving much of the country’s mineral potential untapped (WEF 2025)